Creating your own cryptocurrency is no longer limited to large tech companies or expert developers. With the right knowledge and tools, individuals and businesses can build their own digital currency. Whether you want to power a decentralized app, simplify payments for a community, or launch a new platform, this guide walks you through every key step in plain language.

What Is Cryptocurrency and Why Build One?

Cryptocurrency is digital money secured by cryptographic code. Unlike government-issued currency, it runs on decentralized networks powered by blockchain technology — a shared digital ledger maintained across thousands of computers called nodes.

People and businesses create their own cryptocurrencies for many reasons:

- To simplify transactions within a specific community or platform

- To power a new product, service, or marketplace

- To build a token for a decentralized application (dApp)

- To raise funds through token sales or initial coin offerings

Knowing your purpose from the start shapes every decision you make — from technical design to legal compliance.

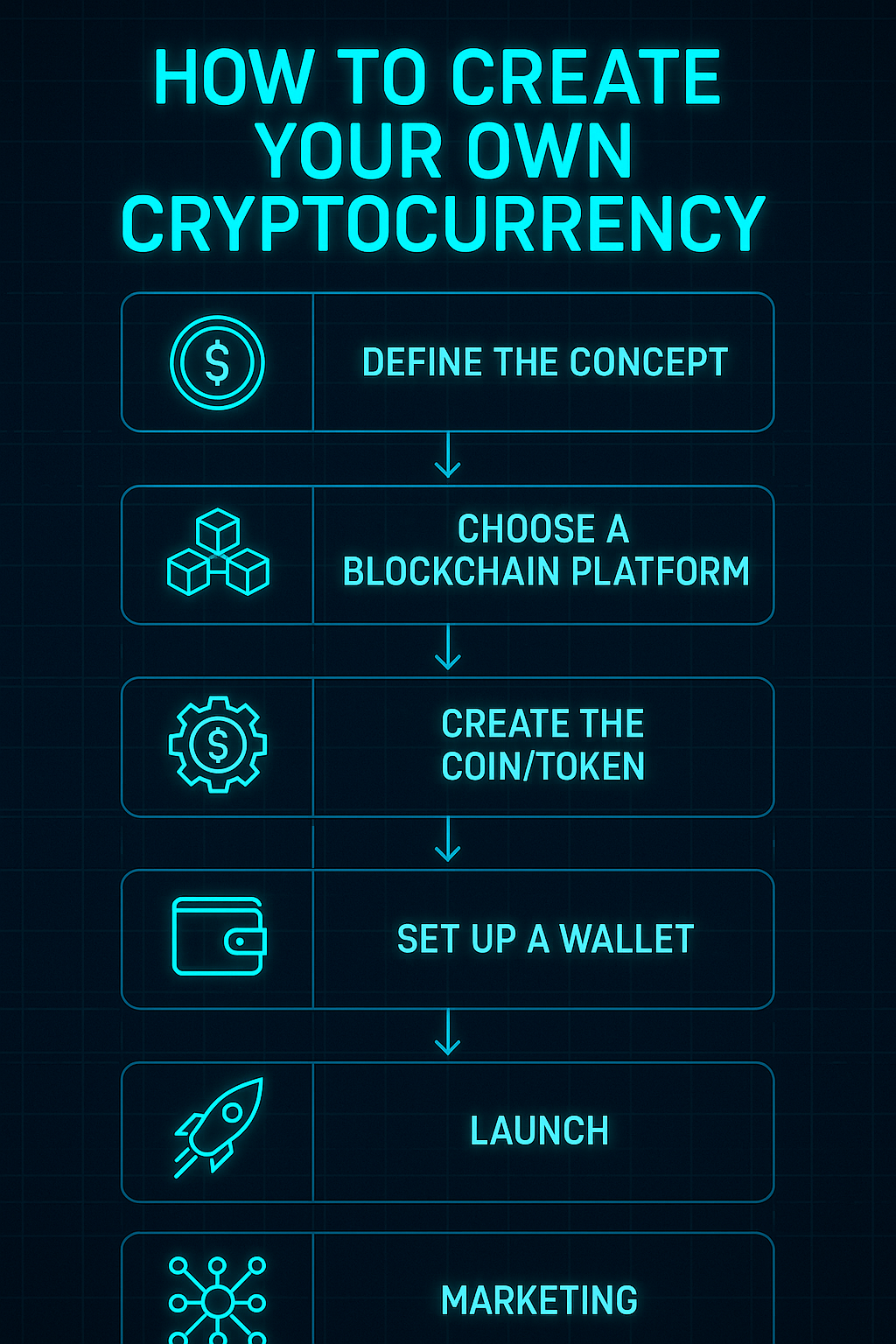

Step 1: Choose Your Blockchain Approach

Your first major technical decision is how you want to build your cryptocurrency. There are three main paths:

| Approach | What It Means | Best For |

|---|---|---|

| Build a New Blockchain | Create a blockchain from scratch | Advanced developers needing full control |

| Fork an Existing Blockchain | Modify the code of Bitcoin or Ethereum | Developers with moderate technical skills |

| Create a Token on Existing Blockchain | Use Ethereum (ERC-20), Binance Smart Chain (BEP-20), or Solana | Beginners and most new projects |

For most beginners, creating a token on an established blockchain like Ethereum or Binance Smart Chain is the fastest and most practical route. It removes the complexity of building infrastructure from scratch.

Step 2: Design Your Cryptocurrency

Once you pick your platform, you need to define the core properties of your cryptocurrency. These decisions affect how it behaves, how it is valued, and how users interact with it.

- Name and Symbol: Choose a memorable name and a short ticker symbol, similar to how BTC represents Bitcoin.

- Total Supply: Decide the maximum number of coins or tokens that will ever exist. A limited supply can create scarcity and value.

- Decimals: Set how many decimal places your token supports, which determines how small a fraction can be transacted.

- Consensus Mechanism: Choose how transactions are verified. Common options include Proof of Work (PoW) used by Bitcoin and Proof of Stake (PoS) used by Ethereum after its upgrade.

- Special Features: Decide if your token can be minted (created over time), burned (permanently removed), or paused in emergencies.

Step 3: Write and Deploy Smart Contracts

Smart contracts are self-executing programs stored on the blockchain. They define the rules of your cryptocurrency — who can transfer it, how new tokens are created, and what happens under specific conditions.

You have two main options for creating smart contracts:

- Write your own code: If you have programming skills, you can write smart contracts using Solidity, the most widely used language for Ethereum-based tokens. This gives you full flexibility.

- Use no-code tools: Platforms like TokenMint and Bitbond’s Token Tool allow you to create tokens without writing a single line of code. These are ideal for non-developers.

Before going live, always test your smart contract on a testnet — a simulated blockchain environment where you can catch bugs without risking real funds. Only after thorough testing should you deploy on the main network.

Step 4: Handle Legal Compliance

Cryptocurrency regulations vary widely across countries. Ignoring legal requirements can result in fines, shutdowns, or criminal liability. Before launching, take these steps seriously:

- Consult a legal expert: Work with a lawyer who understands cryptocurrency and financial regulations in your target markets.

- Understand securities laws: In many countries, tokens that promise returns may be classified as securities and require registration.

- Follow anti-money laundering (AML) rules: Depending on your project, you may need to implement Know Your Customer (KYC) processes.

- Tax obligations: Understand how your token issuance and transactions will be taxed locally.

In India, for example, the government has introduced a 30% tax on cryptocurrency gains and a 1% TDS on transactions, making compliance essential for any Indian project.

Step 5: Launch and Promote Your Cryptocurrency

Technical creation is only half the work. Getting people to use and trust your cryptocurrency requires a strong launch strategy.

- Build a website and publish a whitepaper: A whitepaper explains your project’s goals, technology, and tokenomics in detail. It builds credibility with investors and users.

- Grow a community: Use platforms like Twitter, Telegram, Discord, and Reddit to connect with potential users and supporters.

- List on exchanges: Getting your token listed on decentralized exchanges (DEXs) like Uniswap or centralized exchanges increases accessibility and trading volume.

- Partner with other projects: Collaborations with existing blockchain projects can accelerate adoption.

Building trust takes time. Consistent communication, regular updates, and transparent governance go a long way in establishing your cryptocurrency as a credible project.

Creating your own cryptocurrency is a multi-step process that combines technical work, strategic design, legal awareness, and community building. Whether you are a developer, entrepreneur, or startup founder, the tools and platforms available today make it more accessible than ever. Start with a clear purpose, choose the right blockchain platform, and always prioritize security and compliance before going live.