Sending money across borders has always been a slow, expensive, and complicated process. Whether it is a worker sending remittances back home or a business paying an overseas supplier, traditional international transfers come with layers of fees and delays. Blockchain technology is now offering a faster, cheaper, and more transparent alternative — and it is gradually reshaping how money moves around the world.

What Are Cross-Border Payments?

Cross-border payments refer to any financial transaction where the sender and the recipient are located in different countries. These include:

- Remittances sent by migrant workers to their families

- Business-to-business payments for international trade

- Foreign investments and portfolio transfers

- E-commerce payments to overseas merchants

Traditionally, these payments pass through multiple intermediaries — correspondent banks, currency exchange services, and payment processors — before reaching the recipient. Each step adds time and cost to the transaction.

Problems with Traditional International Money Transfers

The conventional system for cross-border payments has several well-known drawbacks that affect both individuals and businesses:

- High Fees: Multiple intermediaries each charge their own fees, making international transfers significantly more expensive than domestic ones.

- Slow Processing Times: Transfers can take two to five business days due to banking hours, time zone differences, and manual verification processes.

- Lack of Transparency: Tracking a payment in real time is difficult, and hidden charges often appear only after the transaction is complete.

- Currency Exchange Complications: Converting one currency to another introduces additional costs and exposure to fluctuating exchange rates.

- Limited Access: People in countries with underdeveloped banking infrastructure often struggle to send or receive international payments at all.

How Blockchain Technology Addresses These Challenges

Blockchain is a decentralized digital ledger that records transactions across a network of computers. Because no single authority controls it, blockchain can process payments directly between two parties without needing banks or other middlemen. This fundamental difference is what makes it so powerful for international transfers.

Here is how blockchain improves on the traditional system:

- Lower Transaction Fees: By removing intermediaries, blockchain significantly reduces the cost of sending money internationally.

- Faster Settlement: Blockchain transactions can settle in minutes rather than days, improving cash flow for businesses and individuals alike.

- Real-Time Tracking: A shared, transparent ledger allows both sender and receiver to track the payment at every stage.

- Efficient Currency Conversion: Certain blockchain platforms handle currency exchange within the same system, reducing the complexity and cost of conversion.

- Enhanced Security: Cryptographic encryption makes blockchain transactions extremely difficult to tamper with or hack.

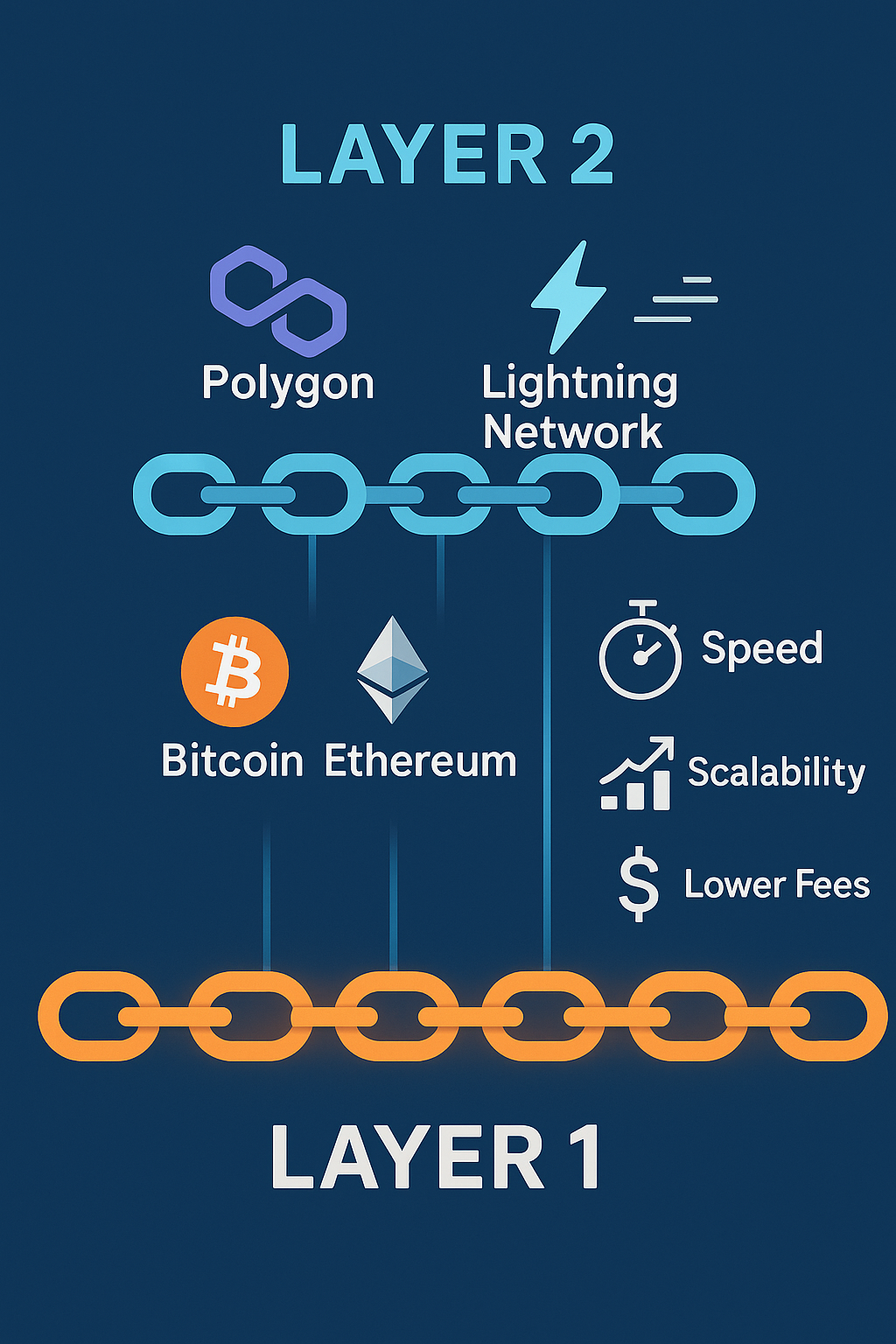

Key Blockchain Technologies Used in Cross-Border Payments

Several specific technologies built on blockchain are already being used to improve international transactions:

| Technology | How It Helps | Examples |

|---|---|---|

| Cryptocurrencies | Enable fast, borderless digital payments without banks | Bitcoin, Ethereum |

| Stablecoins | Offer blockchain benefits with price stability tied to fiat currencies | USDT, USDC |

| Smart Contracts | Automate payment execution, reducing manual errors and costs | Ethereum-based contracts |

Cryptocurrencies like Bitcoin and Ethereum allow users to send value directly to anyone in the world without going through a bank. Stablecoins solve the volatility problem by pegging their value to traditional currencies like the US Dollar, making them more practical for everyday transactions. Smart contracts are self-executing agreements coded on the blockchain that automatically release funds when pre-set conditions are met, removing the need for manual processing.

Benefits of Blockchain-Based Cross-Border Payments for India and Beyond

India is one of the largest recipients of international remittances in the world. Millions of Indians working abroad send money home every year, and high transfer fees eat into a significant portion of those earnings. Blockchain-based payment systems can directly benefit this population by:

- Reducing remittance fees, allowing families to receive more of what is sent

- Speeding up transfers so funds are available almost immediately

- Providing access to financial services for people in rural or underbanked areas

- Giving small and medium businesses a cost-effective way to pay international suppliers

For businesses engaged in global trade, faster settlement times mean better cash flow management and fewer delays in supply chains. The security features of blockchain also reduce the risk of fraud, which is a growing concern in international finance.

What the Future Holds for Blockchain in Global Finance

Blockchain’s role in international payments is still growing. Governments and central banks around the world are exploring Central Bank Digital Currencies (CBDCs), which are government-backed digital currencies built on blockchain-like infrastructure. These could eventually work alongside or replace some existing payment systems.

Financial institutions are also investing in blockchain networks to modernise their own cross-border payment infrastructure. As adoption increases and regulations become clearer, blockchain-based payments are expected to become faster, more accessible, and even more affordable. The technology holds real potential to bring millions of unbanked people into the global financial system for the first time.

In conclusion, blockchain is not just a trend in finance — it is a practical solution to long-standing problems in cross-border payments. From lower fees and faster transfers to greater transparency and security, the advantages are clear. As the technology matures, it is set to become a standard part of how money moves across borders, benefiting individuals, businesses, and economies worldwide.